Adulting Hack: How to Dance in Life’s Storms Without Getting Soaked

Let’s be real—insurance talk can feel like assembling IKEA furniture without instructions. But here’s the good news: you’re not starting completely unprotected in a thunderstorm. Singapore’s already handed you some pretty decent rain gear, and once you learn how to layer up properly, you’ll see that staying dry (financially speaking) totally doable. Think of this as weather forecast — no meteorology degree needed. Just chill vibes and smart rain gear choices.

15 December 2025

SOURCE: CPF Board

First Things First: Rain Gear Isn’t Just for Storm Chasers

“Wealth protection” sounds like something for people who drive fancy cars and fly first class, doesn’t it? At least, that’s what I thought at first as well. But then I came to an epiphany: it’s called wealth protection, not millionaire protection – and I’ve got wealth too, no matter how small!

Here’s what I tell myself: when it rains, you’d naturally protect your phone so it doesn’t get wet and die on you. Whether it’s the latest iPhone or that ancient Nokia that could survive the apocalypse – you’d want to keep your phone dry all the same, because that phone is yours!

At the end of the day, having good rain gear is a way for you to ensure that you still get to do the things you love without getting completely drenched when life decides to pour. You can still splash in puddles and dance in light showers; but it’s also nice to know you won’t catch pneumonia when the real storms hit.

And here’s your first win—you’re already carrying an umbrella called MediShield Life. Even if you haven’t done anything yet, it’s already keeping you dry in the background of your life.

Understand What Weather Gear You Already Have

Before you get tempted by that TikTok ad for fancy health insurance or riders that sound like a great deal, take a sec to understand what you’ve already got.

Singapore’s healthcare system is built on two solid ideas:

- Individual responsibility – We all bring our own umbrellas and check the weather forecast

- Affordable healthcare for all – No one should have to run through storms just because they can’t afford rain gear

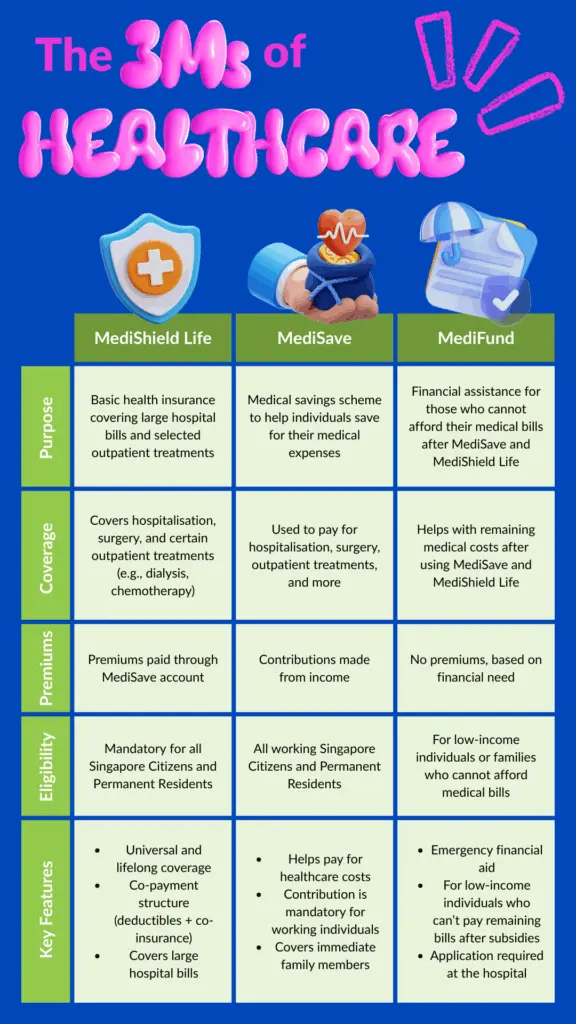

These twin philosophies are backed by three layers of weather protection—MediSave, MediShield Life and MediFund, to better weather the storms that might come your way.

MediSave: Your Trusty Everyday Umbrella

MediSave is your personal healthcare savings account. Every month, a portion of your salary (if you’re working) is automatically saved in this account.

Your MediSave savings are like that trusty compact umbrella that lives in your bag, always ready to protect you against the rain (or sun). But you won’t whip out this umbrella for every tiny sprinkle though. It’s not your all-access pass to flu meds or dental cleanings. Think of it as your go-to protection for the real downpours – hospitalisation, surgery, and certain outpatient treatments – it helps you cover part of these bills before you even touch your bank account.

Your MediSave savings also provide shade on the sunny days – covering vaccinations and health insurance – to keep you protected even when you’re in the pink of health.

Best thing? Unlike an umbrella, your MediSave savings are always growing at a stable interest rate of at least 4% per year!

BARGAIN HUNTER TIP:

You can share this particular umbrella with your parents or siblings when they need medical coverage too.

MediShield Life: Your Basic Raincoat for the Thunderstorms

This is the heavy-duty raincoat that’s always there for all Singapore Citizens and Permanent Residents—no matter your age, job, and income (or umbrella-forgetting habits).

It handles the thunderstorms – big hospital bills and expensive outpatient treatments like dialysis and cancer drugs. It covers most subsidised bills at Class B2 or C wards at public hospitals – think functional raincoat, not designer waterproof fashion. Claim limit: $200,000 per year, with no lifetime cap.

Yes, you still get a little damp (you’ll still have to pay a deductible + co-insurance), but your MediSave savings can help with that. The co-insurance prevents people from abusing the system – can’t have bad apples ruining good rain gear for everyone!

Want private doctors or fancier hospital rooms? That’s where Integrated Shield Plans (IP) come in, which are optional private insurance policies. They’re like adding designer rain boots to your basic outfit. They work on top of MediShield Life for better wards, private hospitals, and higher claim limits. Necessary? Depends if you want premium shelter or if basic coverage keeps you dry enough.

MediFund: When You Can’t Afford to Dry Yourself Off

If you really can’t afford the remaining bill after MediSave and MediShield Life covers the bulk of the bill, MediFund kicks in. It’s designed for low-income individuals who’ve exhausted all other options.

Application for MediFund is straightforward, just talk to the hospital or clinic staff. A committee will then review your financial situation and medical needs, and if approved, the government pays part (or all) of your outstanding bills. So, even if all else fails, Singapore does her best to make sure you don’t end up soaked and miserable.

Let’s take a look at the options you’ve got:

CareShield Life: Because Your Future Deserves a Weather-proof Shelter

This one’s about future-proofing. If (touchwood!) you get severely disabled and can’t perform at least 3 out of 6 activities of daily living (like bathing or walking), CareShield Life gives you monthly cash payouts to help you pay for your long-term care needs.

I know it’s not something we think about when we’re young and feel invincible, but when life decides to throw a monsoon at you (and it might), you’ll be glad you’ve got this shelter. I didn’t feel great myself entertaining these thoughts, but it was comforting to know that even if it does happen, however unlikely, I’d be covered.

What it includes:

- Monthly payouts begin at $689/month and increase annually until age 67 – meaning the older you are when you first make a successful claim, the more you’ll receive each month

- You receive payouts for as long as the severe disability lasts

Premiums?

- You start paying at 30, via MediSave. Payments stop at 67 or when you make a successful claim.

- Want better storm protection? You can get private supplements, which can increase monthly payouts, reduce the disability threshold, provide lump-sum payouts, and/or increase coverage to mild disability.

Government Subsidies: The Unsung Heroes of Affordability

We’re not just relying on our own rain gear here. There are subsidies that help keep healthcare costs manageable.

Examples:

- CHAS (Community Health Assist Scheme): For lower- and middle-income families to get subsidised care at GPs and dental clinics.

- Subsidies at Public Hospitals & Polyclinics: Up to 80% off, depending on income level and ward class

Eligible Singaporeans are automatically enrolled for these subsidy schemes, except for CHAS which requires you to personally sign up for.

Keep Dancing Through the Rain!

Some people say adulting is scary, because you never know when the next downpour will hit. Although that’s true, at least now you know what protection you have to life’s storms!

So what’s next? Here’s how to level up your weather game:

- Explore Integrated Shield Plans: If you want premium rain gear, use the Health Insurance Planner to easily see compare the Integrated Shield Plans in the market.

- Look into CareShield Life supplements: For extra long-term care payouts.

- Talk to financial advisers: They’re the weather experts, and they can elaborate on various life, critical illness and accident insurance plans that can alleviate your healthcare concerns.

Because wealth protection isn’t about hiding indoors—it’s about being able to dance in the rain without worry. And when you know life’s storms won’t leave you shivering and broke, that’s when you can really start splashing through puddles and enjoying every season.

You got this weather warrior,

The Wonder Guide

The information provided in this article is accurate as of the date of publication.

You might also be interested in…