Destination: Family Security – Pack the Right Money Moves for Life’s Adventures

Just like planning the perfect family getaway, smart financial planning is about knowing your resources. With the right strategies, you can prepare your family for life’s adventures without breaking the bank.

15 December 2025

SOURCE: CPF Board

When dreaming of your next family trip, you probably start with a wishlist – where to go, what to do, memories you want to create. You know budget matters, but there’s something to be said for dreaming a little before crunching the numbers.But just like that unexpected baggage fee at the airport, financial realities have a way of catching up with us. The same applies to managing your family’s expenses and future security.

We all know life isn’t cheap, especially with a family in tow.

But drastic lifestyle changes aren’t always the answer. Think of it like travel planning – stretching your budget doesn’t mean you have to give up on the destinations you’ve been dreaming of; you just need to plan smarter and know what resources are available to you.

CPF Top-Ups: Your Family’s Financial Passport to Security

Remember being a kid on family holidays when your parents covered all the costs? They were essentially “topping up” your share of the adventure. You can do the same for your family with CPF – and like before, you get the benefits too.

Under the Retirement Sum Topping-Up (RSTU) Scheme, cash top-ups to your loved ones’ Special or Retirement Accounts can earn you up to $8,000 in tax relief per year. You can enjoy this relief when you top up for your parents, parents-in-law, grandparents, grandparents-in-law, spouse or siblings – provided their annual income doesn’t exceed $8,000.

Here’s the simple version:

- If family member’s annual income < $8,000/year, your top-up gives you up to $8,000 in tax relief

- It lowers the amount of income you’re taxed on – a win-win for you and your family

But wait, there’s more. You can enjoy another $8,000 in tax relief when you top up your own Special or Retirement Account. That’s potentially $16,000 in total relief each year.

This also helps your savings grow faster (up to 6% per year thanks to the Special Account’s interest rates) whilst boosting your future retirement income. It’s like stamping your passport to a more secure financial future.

Seniors under the Matched Retirement Savings Scheme can enjoy up to $2,000 per year in matching grants when they receive these top-ups – think of it as bonus miles for good financial planning.

Topping up is straightforward via the CPF Mobile app or online form. You’ll need basic details like NRIC name and number – way easier than booking flights online. Just remember: CPF top-ups are irreversible, so carefully consider the amount you want to transact before you do so.

Check the Retirement Dashboard, to see how much you can top up and your remaining tax relief for the year.

Group Bookings for Better Value: Optimise Your Subscriptions

Just like group tour packages offer better value than individual bookings, family subscription plans can stretch your entertainment budget further whilst reducing forgotten payments.

Take inventory of your current subscriptions. How many are you actively using? Forgotten subscriptions are like paying for hotel rooms you never sleep in – pure waste.

Group subscriptions solve two problems: they’re cheaper per person and less likely to be forgotten since multiple family members are invested. For mobile data and streaming platforms, consolidating into family plans can deliver significant savings.

Have you reviewed your family’s subscription landscape recently? It might be time for some smart consolidation.

Your Home Base: Maximising Housing Subsidies and Smart Planning

Buying a home is like choosing your family’s permanent base camp, it deserves careful planning. Just like you wouldn’t blow your entire holiday budget on a fancy hotel and have nothing left for activities, don’t stretch yourself so thin on your home purchase that you’ve got nothing left for life’s other essentials, like retirement and emergencies.

Before you start on your house-hunting journey, here’s the essential pre-departure checklist you need, to have a clear plan in mind:

- Why now? Are you upgrading for more space, better location, or investment? Make sure the timing makes sense for your family’s situation and needs.

- What can you actually afford? Factor in down payment, monthly instalments, and still having enough left over for daily expenses, emergencies, and life’s little treats. Research available home loan options and determine which suits your family best. You can pay with cash, your CPF savings, or both (preferably both for maximum flexibility). If you’re intending to use your CPF savings for housing, then familiarise yourself with the CPF housing refund process and how withdrawals will impact your retirement savings.

- What help is available? There are grants designed specifically to ease the burden – might as well use them.

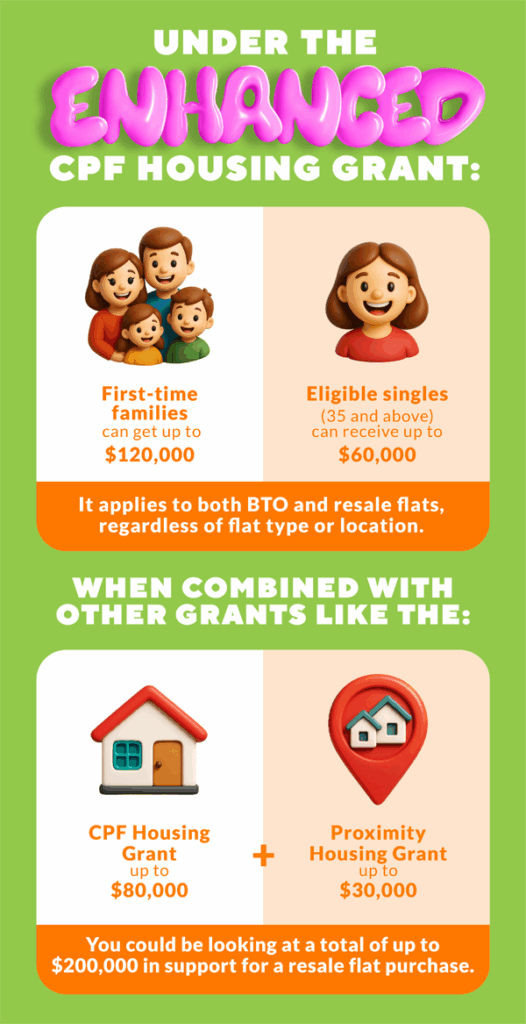

Through the Enhanced CPF Housing Grant (EHG) first-time flat buyers can enjoy up to $120,000 in grants, whilst singles receive up to $60,000. Monthly household income must not exceed $9,000 (or $4,500 for singles aged 35 and above), with 12 months of continuous employment required.

Stack this with other grants such as the CPF Housing Grant for Resale Flats (up to $80,000) and Proximity Housing Grant (up to $30,000 if you’re buying near family) and you could be looking at up to $200,000 in support. That’s a significant chunk of your down payment sorted. Find more information on all grants here.

PRO TIPS:

- Keep your monthly housing loan within what your Ordinary Account monthly contributions can cover. This way, your take-home pay stays intact for everything else your family needs. And don’t skip the Home Protection Scheme, for your family’s peace of mind.

- Before you embark on this big journey, be sure to use the Home Purchase Planner to crunch the numbers. Better to know your limits upfront than get your hopes up only to realise it’s out of reach.

Protecting Your Travel Companions: Legacy Planning

Your CPF savings aren’t just about building your nest egg – they’re also about making sure your family is taken care of if something happens to you. Think of CPF nomination like updating your emergency contacts before a big family trip – it’s one of those “just in case” things that you hope you’ll never need, but you’ll be glad you sorted it out.

When you make a CPF nomination, your savings get distributed directly as cash to your chosen beneficiaries – quickly and without administrative fees eating into what you’ve left for them. Without a nomination, your family might face delays and additional costs during an already difficult time.

Even if you’ve already made a nomination, life changes mean you should review it regularly. By the way, got married recently? Congratulations – but heads up, marriage automatically cancels any existing nomination.

Take 10 minutes to make or update your CPF nomination. It’s like leaving clear instructions for your family about where you’ve packed the important stuff – except in this case, it’s your life’s savings.

You can sort this out online through the CPF website – no need to take time off work or queue anywhere.

For seniors or those with health concerns, consider engaging a lawyer for a Lasting Power of Attorney (LPA) and will. An LPA enables a trusted person to make decisions if you become incapacitated – like having a reliable travel companion who can take charge when needed.

Securing Your Family’s Future Starts Today

Your family’s financial journey begins with a single step. Pick one strategy from this travel kit and start today.

Safe travels,

The Safe Beacon

The information provided in this article is accurate as of the date of publication.

You might also be interested in…