Simple Saving Tips for Growing Your Money

If your bank balance feels lower than it should, you might be leaking money without realising it. Here’s how to spot and patch those leaks – think of it as decluttering your digital shopping cart, but for your entire financial life.

15 December 2025

SOURCE: CPF Board

You know that moment when you’re about to check out online (or right after, when you open your banking app to inspect the damage), and your bank balance looks… wrong? Like, you were supposed to have way more money than what’s actually there? Yeah, we’ve all been there.

Money leaks the same way our online shopping carts mysteriously fill up. Good news though – plugging these leaks doesn’t mean some dramatic ‘no fun allowed’ lifestyle overhaul.

All you need to do is be a little more intentional, so that you can keep your comfort, your treats, and your peace of mind for rainy days. A few minutes of due diligence = huge savings.

Here’s how I freed up cash (which I admittedly promptly spent on things I actually use).

Scrutinise Your Subscriptions

Remember when you signed up for that meditation app during a particularly stressful work week? Or that premium music streaming service because they offered a free trial? Yeah, about that…

I checked my bank statement and realised that I was paying for subscriptions I literally forgot existed. It’s like having items sitting in your cart for months – except these ones auto-checkout every month!

The lesson that I learned? Subscriptions are designed to be easily forgotten No physical product cluttering your desk means nothing reminding you they exist.

Now I’m wiser and a tad bit richer! Here’s what I did:

- First, do a subscription audit. Open your banking app right now – yes, now – and check what’s auto-charging you monthly. Not using it? Unsubscribe. Pro tip: Unsubscribe BEFORE you uninstall the app, or you’ll forget it exists while it keeps charging you.

- Compare monthly vs annual plans. Some services are cheaper if you pay upfront for the year. If you’re definitely keeping it, this is basically a discount for committing.

- Check your employee benefits. You might be eligible for discounts you didn’t know about.

- Good things must jio. Family plans are usually cheaper than going solo. Get your siblings or housemates in on it—everyone saves.

- Set a reminder. Set a quarterly calendar reminder review your subscriptions. You’ll be glad when you catch that gym membership that you haven’t used since CNY.

ONE THING TO DO RIGHT NOW:

Open your banking app, scroll through last month’s transactions, and cancel ONE subscription you’re not using. Done? Nice. Go back to your show.

Browse for Better Deals

You already know how to comparison shop online. Now apply that same energy to everything else:

- Compare ride-hailing apps: The first one you open is not always the cheapest. It takes 30 seconds to check other apps and can save you a few dollars per trip

- Price compare the big stuff: Why stop at comparing ride-hailing apps? For expensive purchases like electronics or furniture, spend five minutes checking a few sites. Same effort as scrolling social media, except you save a few hundred dollars.

- Hunt for discounts: Never pay full price if you don’t have to.

- Try cheaper alternatives: If you can’t tell what’s different about a famous brand besides its price tag, might as well try something cheaper.

Watch Out for Bad Debt

Collecting stuff is cool and all, but collecting bad debt? Don’t start.

Look – not all debt is bad. Debt that helps you gain more financial security in the long run (home loans; business loans; education loans) are okay. But loans to buy a car, that latest fashion item, that fancy renovation, or non-essential goods are dangerous territory. These can accumulate fast – like items mysteriously multiplying in your shopping cart on 11/11.

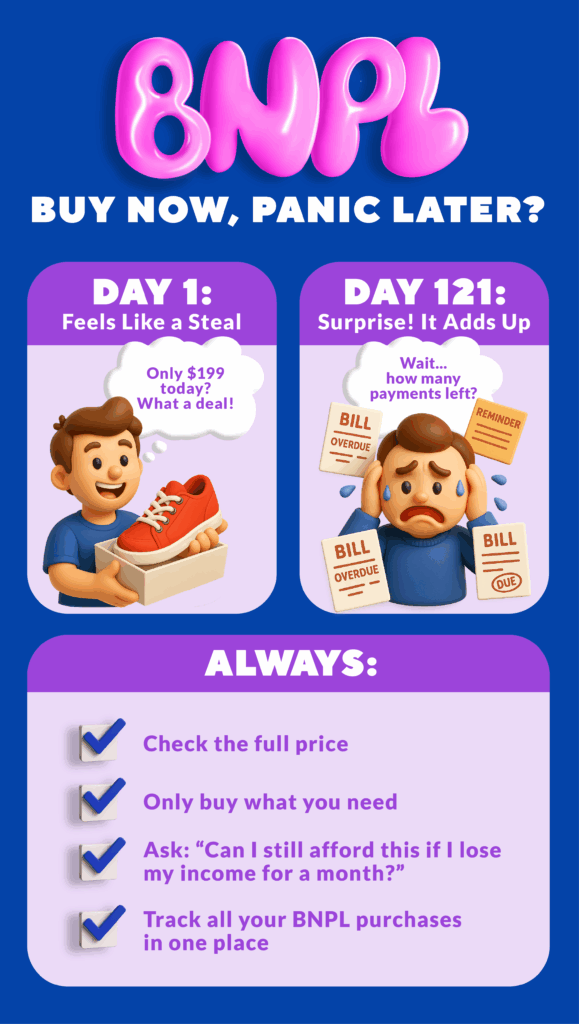

Buy Now, Pay Later (BNPL) is everywhere now, and it’s dangerously easy to use. You see something you want, split it into 4 payments, and boom – it’s yours. Except we tend to focus on the first payment and forget about the other three.

BNPL reality check:

- Check the full cost before checkout – not just the first instalment. Can you afford it?

- Only say yes to BNPL if it’s for genuine needs, or legit discounts. If you’re using BNPL for because you can’t afford something right now, you probably can’t afford it instalments either.

- Track all payments: Mark them in your calendar. Set reminders. Treat them like bills, because that’s what they are. That BNPL payment that started 3 months ago – and that one that started 5 months back – can you afford to pay for these instalments on top of the next BNPL buy?

Read the truth about BNPL here.

GOLDEN RULE:

If it’s not in your budget, it shouldn’t be in your cart.

Make Extra Cash Work Harder

Got some extra money lying around? Before you spend it on yet another online purchase, here are two smarter places to park that cash:

- Start a ‘fun fund’: Set up a separate digital wallet for your hobbies and treats, and when you get extra cash – bonus, ang bao, that refund you forgot about – put it there. Now you can spend guilt-free because it’s already budgeted.

- Top up your CPF accounts: Okay hear me out – your CPF account is the one friend who’ll help you buy a home, afford healthcare, and retire with financial security. So if you have spare cash, top up your CPF account to take advantage of the good interest rates (up to 5% at our age), and let your CPF savings grow to meet your key needs.

PRO TIP:

Yup, “saving money” sounds boring and involves effort. But set up recurring transfers, and watch your savings grow while you go back to doing whatever you were doing. Check out how to make recurring top-ups to your CPF account here.

Renovate Smart

We all want that Instagram-worthy home. But unless you’ve got influencer budget, you’ll probably need to pace yourself.

- The places where you spend the most time – perhaps your bedroom and bathroom – are likely your must-haves. All else? Well, they can wait until you’ve got budget left over.

- Don’t spend more than 6x your monthly household income on renos (or 12 months of rental income if you’re a landlord). Think minimalist chic, not maximalist broke.

- Set a firm budget with your contractor, and make sure they are reputable. Real talk: Contractors with rates that seem impossibly low might be moonlighting without proper insurance. It’s like buying that “designer” bag for $50 – yeah it’s cheap, but there’s a reason.

- Avoid renovation loans if you can. While housing loans help you own an asset that can be monetised, renovations don’t always add equivalent value to your property (after all, what looks good to you may not look good to the next owner) and often come with higher interest rates. If you can’t afford your reno without a loan, you probably can’t afford it yet.

Are You Ready to Checkout?

Smart spending isn’t about finding the cheapest option every time – it’s about knowing your bank balance will survive after you hit “buy”. Think of your finances like your online shopping habits: you wouldn’t keep adding items to cart without checking the total, right? Same energy applies to subscriptions, BNPL plans, and all those small charges that add up.

Once you’ve cleared out the unnecessary stuff and kept only what you actually use, you’ll have money to chase the chill. Be intentional, be smart, and maybe – just maybe – check your bank balance before your next impulse purchase.

Say hello to actual savings!

The Chill Conscience

The information provided in this article is accurate as of the date of publication.

You might also be interested in…