Weather-Proofing Your Life: A Chill Guide to Not Getting Soaked

You don’t need to give up your comfort or take giant financial leaps to protect what matters. No pressure, no lecture, no staying up till 3am research insurance policies; just a few easy steps your future self might thank you for.

15 December 2025

SOURCE: CPF Board

Let’s be real – most of us new to the workforce aren’t exactly losing sleep over insurance plans or medical bills. I certainly didn’t. Between figuring out office politics, surviving on instant noodles, and pretending we know what we’re doing in Zoom meetings, why add more stress?

But then, I asked myself: why can’t I enjoy life now and have my future covered at the same time? I’m not gonna shortchange myself on tea runs, so why compromise my future self?

Protecting your wealth now isn’t about giving up the good stuff – it’s about making sure you can keep enjoying it even when life decides to rain on your parade. Simply put, it’s about picking the right weather gear before you need it. Because nobody wants to get caught in a downpour in their newest fancy sneaks and no way to protect them.

The Basics: What’s Wealth Protection Really About?

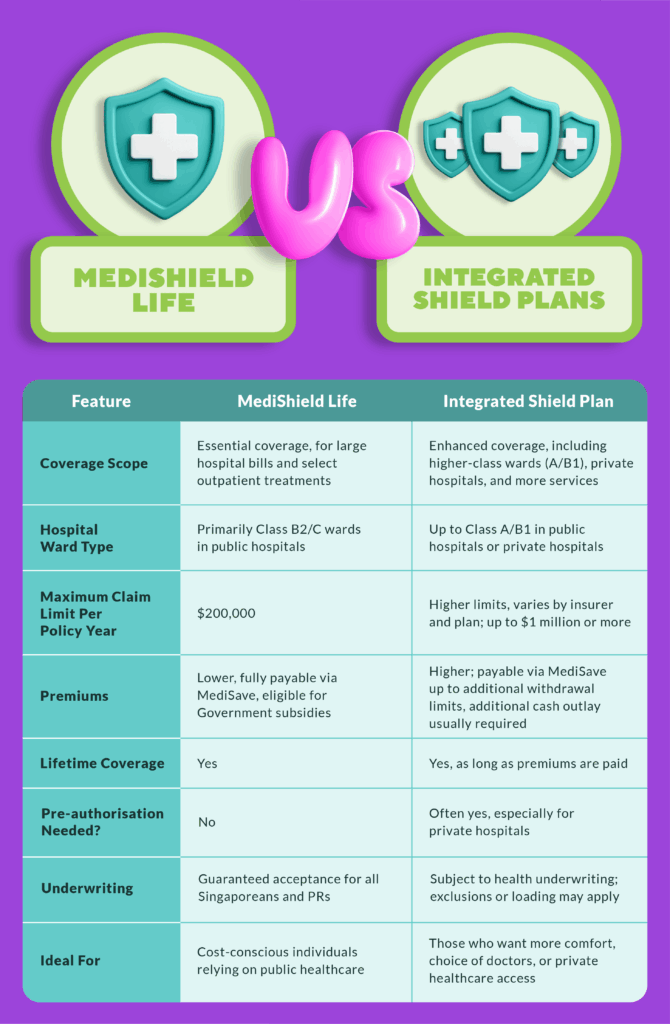

Good news: you’re already equipped with Singapore’s equivalent of a trusty umbrella – MediShield Life. It’s our national health insurance scheme that covers Singaporeans and Permanent Residents for life, handling big hospital bills and certain outpatient treatments like dialysis or chemo. It’s the no-frills, behind-the-scenes MVP of our healthcare safety net.

Coverage focuses on Class B2 and C wards in public hospitals. So if you’re cool with subsidised care and don’t mind sharing a hospital room with others, you’re covered. Best part? Premiums get auto-deducted from your MediSave account, so zero admin headache.

It’s the sturdy umbrella that’s always in your bag—you might not think about it much, but when the rainy days hit, you’ll be glad it’s there. With MediShield Life being there for you from day one, you already have that solid foundation to build on.

Want an Upgrade? Integrated Shield Plans Might Be Your Vibe

Now, if you’re someone who’d rather have a bit more atas care, like single-bed wards, being able to choose your own doctor, or private hospitals, then Integrated Shield Plans (IPs) could be worth considering. IPs layer on top of MediShield Life and let you choose your care level – like upgrading from a basic umbrella to one of those fancy ones with wind resistance and UV protection.

The CPF Health Insurance Planner is a pretty useful tool for comparing IP options without the headache. Explore the options there to see what fits both your wallet and your wish list.

And since it’s important, it bears repeating: it’s about picking the right fit for your needs: don’t be busting out a typhoon shelter when all you really want is an umbrella.

What’s Your Hospital Style?

Since we’re talking about healthcare cost protection, let’s talk some real numbers.

Singapore’s public hospitals offer various ward classes, kind of like choosing between a plain raincoat vs a designer mackintosh – both keep you dry, but one comes with style points and a bigger price tag.

Here’s a rough breakdown of what to expect:

So, what’s your vibe? If you’re fine with the hostel experience and can handle Singapore’s heat without aircon (respect), Class B2 offers solid value. But if you’d rather have more privacy, Class A might be more your style—just be prepared to pay for it.

Keep in mind that these are only ward charges – hospital bills come with a whole host of other charges – including doctors’ fees, test fees and treatment charges, and these can really add up quickly.

Real-Life Example:

Say you need your appendix out (which can literally happen to anyone – thanks, human biology). A hospital stay could potentially cost*:

- B2 ward: $2,892

- A ward: $8,831

- Private hospital: $23,576

* Includes ward charges, doctor’s daily attendance and consultation fee, consumables, medication, tests, accident & emergency charges etc., where applicable. Source: https://www.moh.gov.sg/managing-expenses/bills-and-fee-benchmarks/cost-financing/tosp-sf849a-bill-information/

So, know what you’re paying for, and plan for the level of care you’d realistically want—before you’re groggy and in a hospital gown.

Future Planning = Less Future Stress

Here’s the part many people overlook: insurance premiums increase as you age (just like how my tolerance for all-nighters mysteriously decreased after I turned 25). This means that while you might not feel the pinch now, it’s worth thinking ahead.

Starting early locks in lower rates while you’re still young and (relatively) healthy.

Some things to note:

- MediShield Life premiums are chill and fully covered by your MediSave savings.

- For IPs, only part of the premium is covered by your MediSave savings. The additional private insurance component? That’s only covered up to a certain limit.

It’s About Balance

Start by asking yourself: What kind of hospital stay would I realistically be okay with? Do I want the flexibility of private care down the road, or am I cool with subsidised care for now?

These aren’t quite life-or-death decisions – they’re more like “do I want to carry an umbrella or do I want an umbrella, wellies, and a raincoat too” decisions. You’ll be fine either way, but one option could potentially keep you more comfortable.

Then the next question is: How much would I be comfortable paying for insurance yearly?

Your wallet’s comfort range is important too – all your insurance plans put together should generally stay well within 15% of your take-home pay. Enough so you sleep soundly at night, and not so much that you lay awake sweating about the premiums.

The Takeaway: Small Steps, Big Peace of Mind

No need to go full financial planner mode or start colour-coding spreadsheets (unless you just like spreadsheets). Just getting familiar with options like MediShield Life and Integrated Shield Plans puts you ahead of most people our age who think “insurance” is just something their parents nag about.

So here’s a simple checklist for you:

- Ask yourself the questions I’ve suggested above

- Check out the Health Insurance Planner to see which IP works for you (if any)

- Get protected with the plan that suits you, so that when storm clouds gather, you’ll have the right gear to keep doing your thing instead of running for cover

- Get back to chasing the chill: next time you step out into cloudy skies, you’ll have the right umbrella by your side

Here’s to staying dry and keeping your vibe intact!

The Chill Conscience

The information provided in this article is accurate as of the date of publication.

You might also be interested in…